Market Flash Report | February 2024

Economic Highlights

United States

- The January employment report blew past expectations with 353,000 new jobs added to the economy. The unemployment rate held steady at 3.7% and average hourly earnings surged 0.6% M/M or 4.5% Y/Y. The December report was also revised higher.

- The Personal Consumption Expenditures (PCE) Price Index rose 0.3% M/M or 2.4% Y/Y. Core PCE increased 0.4% M/M or 2.8% Y/Y. Both were in line with expectations. This report eased nerves over the hotter-than-anticipated Consumer Price Index (CPI) report released in mid-February. Inflation remains above the Federal Reserve’s 2% target, but the overall trend is down. Markets continue to expect ~4 rate cuts this year, slightly more than the Fed’s dot chart.

- After surging 4.9% in Q3, the U.S. economy posted 3.2% growth in Q4, according to an updated reading. The update mostly reflected a downward revision to private inventory investment that was partly offset by upward revisions to state and local government spending and consumer spending. Consumer spending grew 3% in Q4, slightly ahead of the 2.8% initial reading.

- Orders for durable or long-lasting goods fell 6.1% in January, but the decline was exaggerated by a brief lull in orders for Boeing passenger planes. New orders fell by a mild 0.3% last month if planes and cars are stripped out. A key measure of business investment, meanwhile, was basically flat. So-called “core orders” edged up 0.1% in January.

- Retail sales declined 0.8% in January after a downwardly revised 0.4% gain in December. The pullback was considerably more than anticipated and even retail sales ex-autos fell 0.6%. Sales at building materials and garden stores were especially weak, sliding 4.1%. Miscellaneous store sales fell 3% and motor vehicle parts and retailers saw a 1.7% decrease. Gas station sales also declined 1.7%. On the upside, restaurants and bars reported an increase of 0.7%. Inflation may have eaten into retail sales.

- The Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) came in below expectations for February at 47.8. New orders, employment and production all softened.

Non-U.S. Developed

- Business activity in the euro area fell at the slowest rate for eight months in February, as a stabilization of output in the service sector offset a further steep downturn in manufacturing. The composite PMI reading of 48.9 was higher than January’s 47.9. Manufacturing fell to a 2-month low of 46.1 and services hit a 7-month high of 50.0. By country, a deepening contraction in Germany and sustained output fall in France were countered by faster growth in the rest of the region. Right now, manufacturing and Germany are drags on the eurozone economy.

- Inflation in the eurozone declined from 2.9% in December to 2.8% in January. Core inflation fell for the sixth straight month to 3.3%, the lowest level since March 2022. The unemployment rate in the eurozone held steady at 6.4% for December.

- Japan's GDP unexpectedly shrank 0.1% Q/Q in Q4 2023, missing market forecasts of a 0.3% growth and following a revised 0.8% fall in Q3. The economy fell into a recession for the first time in five years, as private consumption, which accounts for more than half of the economy, declined for the third successive quarter amid elevated cost pressure and lingering global headwinds. Despite the weak GDP reading and increase in inflation, equity markets have reacted favorably, surpassing the 1989 highs.

Emerging Markets

- China's consumer prices fell by 0.8% Y/Y in January 2024, the most in more than 14 years and worse than market forecasts for a 0.5% fall. It was the fourth straight month of decline in CPI, the longest streak since October 2009. Core consumer prices, which exclude prices of food and energy, increased by 0.4% Y/Y in January, the weakest rise since last June.

- China announced its largest-ever reduction in the benchmark mortgage rate on February 20, as the government sought to prop up the struggling property market and broader economy. The 25-basis-point cut to the five-year loan prime rate (LPR) was the largest since the reference rate was introduced in 2019. Property markets in China are in disarray and mortgage rates are generally too high for people to purchase new homes. Recent deposit rate cuts and the reduction of bank reserves are giving commercial banks space to reduce borrowing costs to support the economy.

- India’s growth is real and growing sharply compared to other developed and emerging market countries. Ten years ago, India ranked as the ninth largest economy in the world, but has grown to be the fifth, with nominal GDP of $3.4 trillion. Jefferies forecasts India’s GDP to reach $5 trillion within the next four years, aiming for nearly $10 trillion by 2030. This fiscal expansion is supported by an anticipated annual GDP growth rate of 6% over the next five years, surpassing the growth rates of most large economies.

- The growth of India’s economy is primarily due to a range of reforms implemented under Prime Minister Narendra Modi’s leadership. These reforms have fundamentally altered India’s economic environment, boosting its stability and appeal to international investors. Notable among these reforms is the introduction of the Goods and Services Tax, which unified the country’s tax regime, simplifying business operations nationwide. Additionally, the enactment of new bankruptcy laws has made resolving insolvency more efficient, while the demonetization campaign was designed to tackle corruption and reduce the prevalence of illicit money.

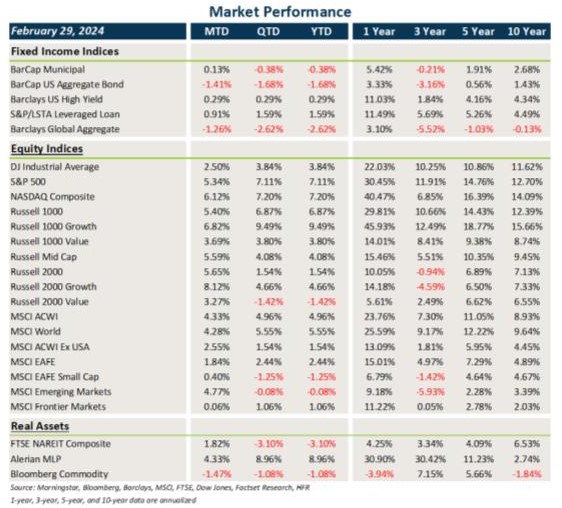

Market Performance (as of 02/29/24)

Fixed Income

- Treasury and other sovereign debt yields rose across the board in February, creating a headwind for core fixed income. Municipal bonds held in better due to favorable technicals.

- Credit bucked the trend with gains in floating rate loans and high yield. Spread tightening occurred within HY, IG and EMD securities.

- U.S. dollar strength acted as another headwind against non-U.S. assets.

U.S. Equities

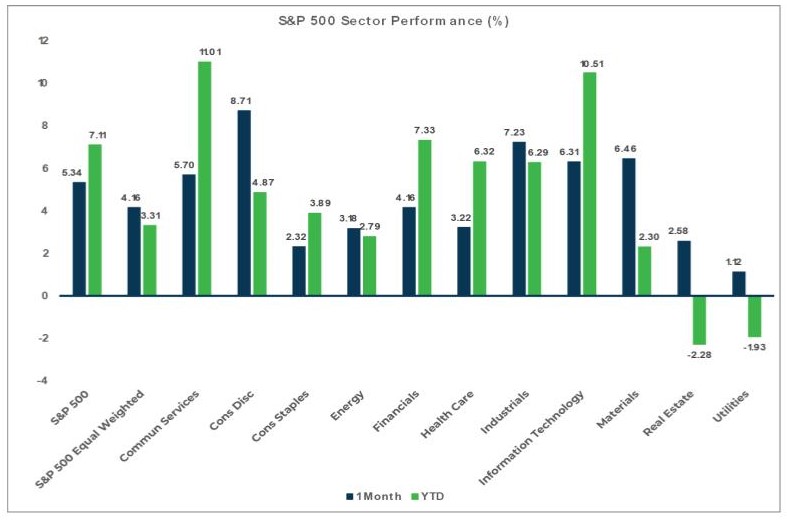

- The equity market rally broadened out in February, similar to what occurred at the end of 2023.

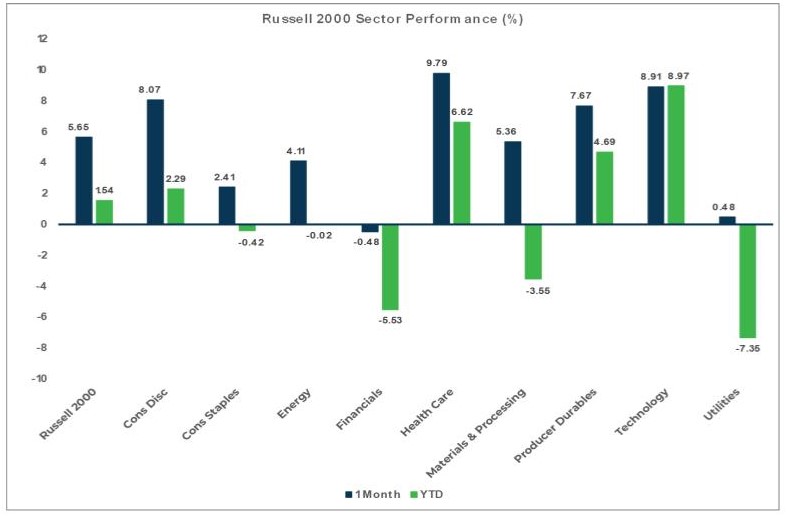

- Small caps led large caps in February and growth trounced value across the entire market cap spectrum.

- Outside of small cap value, all other segments of U.S. equities are positive in 2024.

Non U.S. Equities

- Non-U.S. equities posted positive returns last month, but they lagged their U.S. counterparts.

- Similar to the U.S., large caps outperformed small caps and growth beat value.

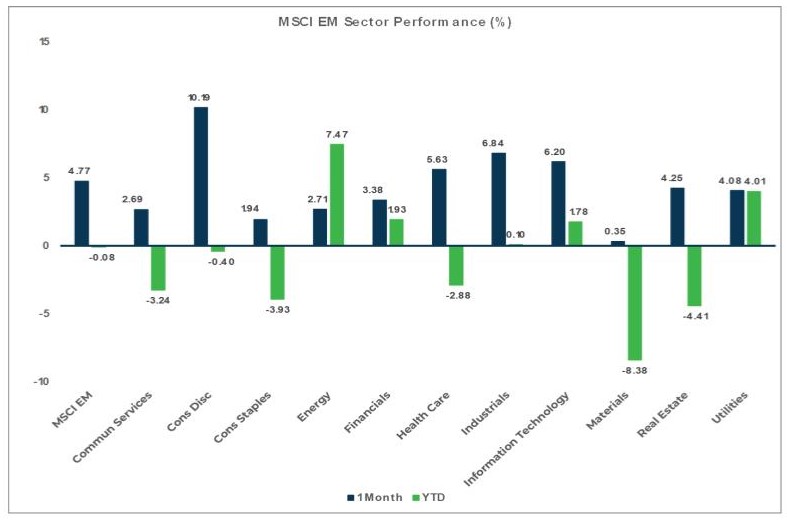

- For the first time in months, emerging markets outperformed other developed markets, largely due to the strong rebound in China.

Sector Performance - S&P 500 (as of 02/29/24)

Sector Performance - Russell 2000 (as of 02/29/24)

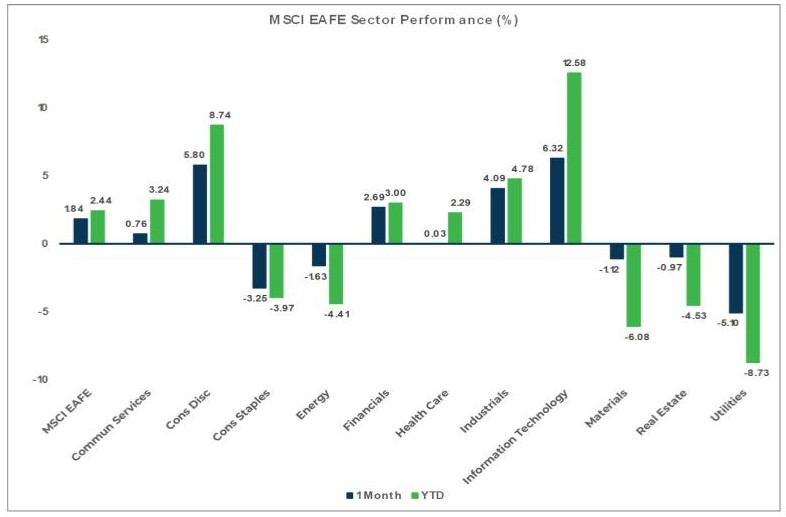

Sector Performance - MSCI EAFE (as of 02/29/24)

Sector Performance - MSCI EM (as of 02/29/24)